Domain name registry operator Verisign (NASDAQ:VRSN) will be announcing earnings results tomorrow after market close. Here’s what investors should know.

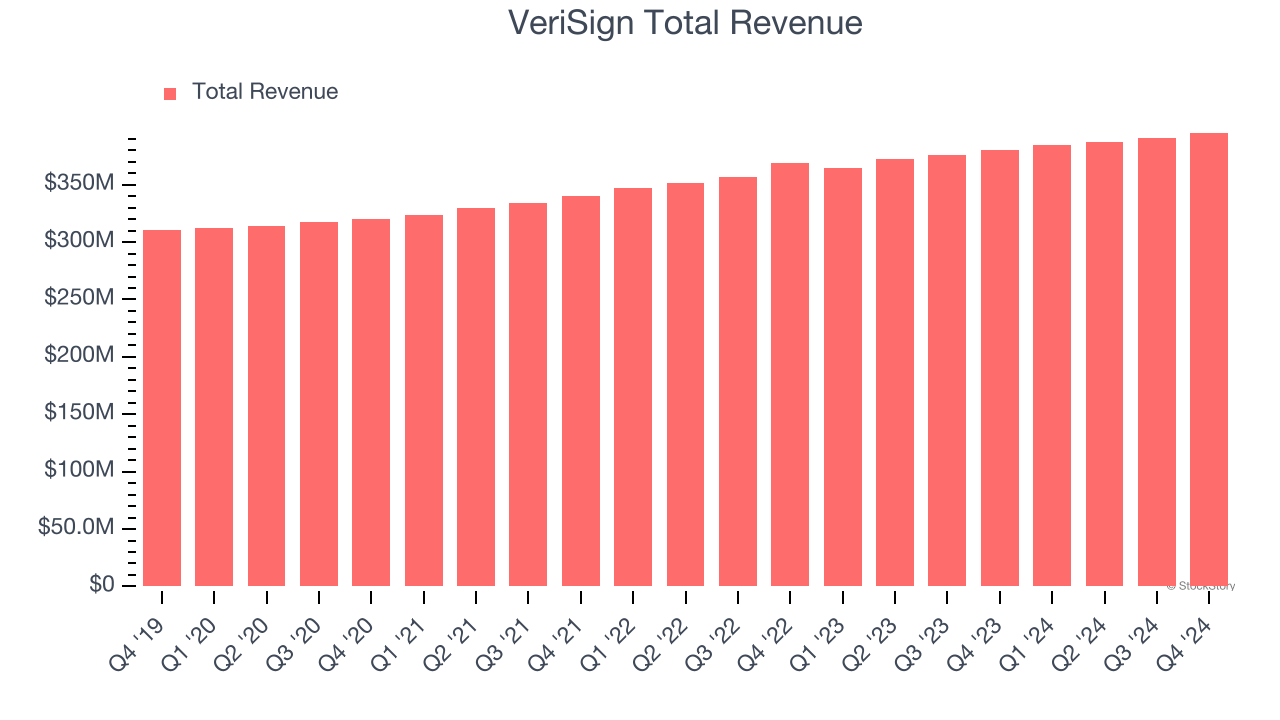

VeriSign met analysts’ revenue expectations last quarter, reporting revenues of $395.4 million, up 3.9% year on year. It was a mixed quarter for the company.

Is VeriSign a buy or sell going into earnings? Read our full analysis here, it’s free.

This quarter, analysts are expecting VeriSign’s revenue to grow 4.2% year on year to $400.4 million, slowing from the 5.5% increase it recorded in the same quarter last year. Adjusted earnings are expected to come in at $2.10 per share.

Analysts covering the company have generally reconfirmed their estimates over the last 30 days, suggesting they anticipate the business to stay the course heading into earnings. VeriSign has missed Wall Street’s revenue estimates three times over the last two years.

With VeriSign being the first among its peers to report earnings this season, we don’t have anywhere else to look to get a hint at how this quarter will unravel for sales and marketing software stocks. However, the whole sector has been hit hard over the last month as stocks in VeriSign’s peer group are down 11.9% on average. VeriSign is up 1.4% during the same time and is heading into earnings with an average analyst price target of $235.28 (compared to the current share price of $249.18).

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.