Security hardware provider Allegion (NYSE:ALLE) beat Wall Street’s revenue expectations in Q1 CY2025, with sales up 5.4% year on year to $941.9 million. Its non-GAAP profit of $1.86 per share was 11.2% above analysts’ consensus estimates.

Is now the time to buy Allegion? Find out by accessing our full research report, it’s free.

Allegion (ALLE) Q1 CY2025 Highlights:

- Revenue: $941.9 million vs analyst estimates of $923.1 million (5.4% year-on-year growth, 2% beat)

- Adjusted EPS: $1.86 vs analyst estimates of $1.67 (11.2% beat)

- Adjusted EBITDA: $228 million vs analyst estimates of $215.6 million (24.2% margin, 5.8% beat)

- Management reiterated its full-year Adjusted EPS guidance of $7.75 at the midpoint

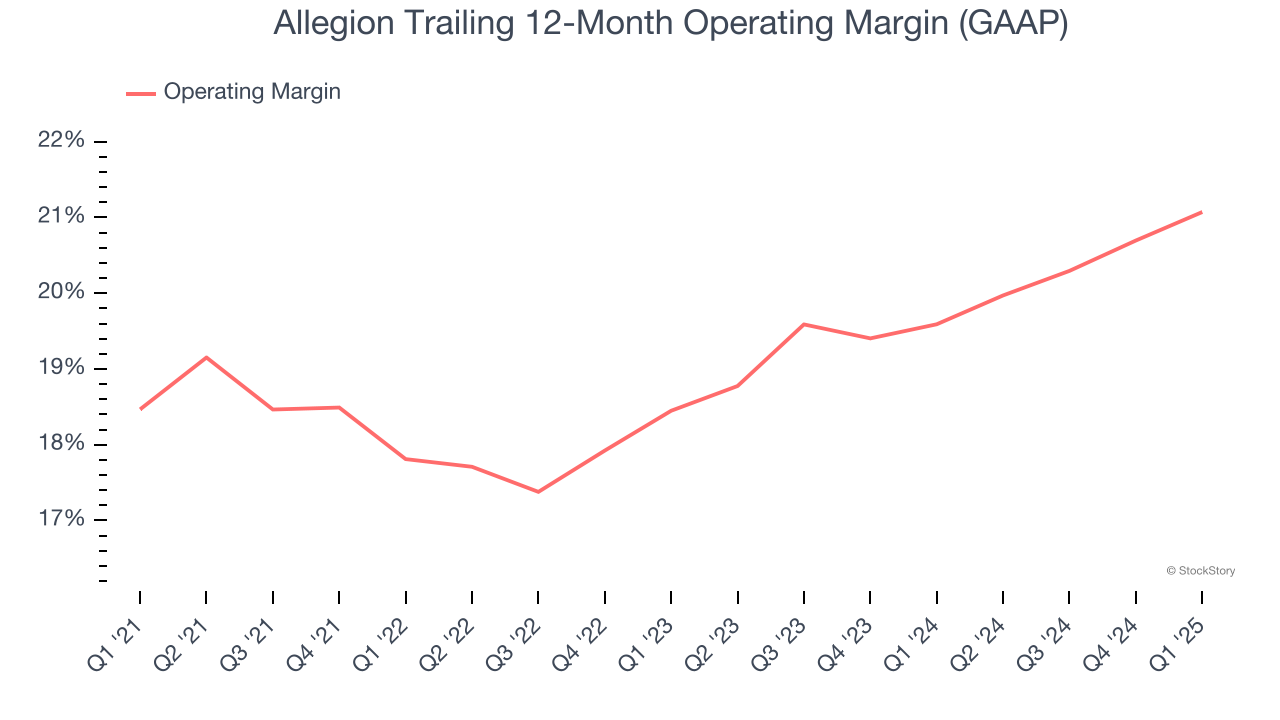

- Operating Margin: 20.9%, up from 19.3% in the same quarter last year

- Free Cash Flow Margin: 8.9%, up from 2.7% in the same quarter last year

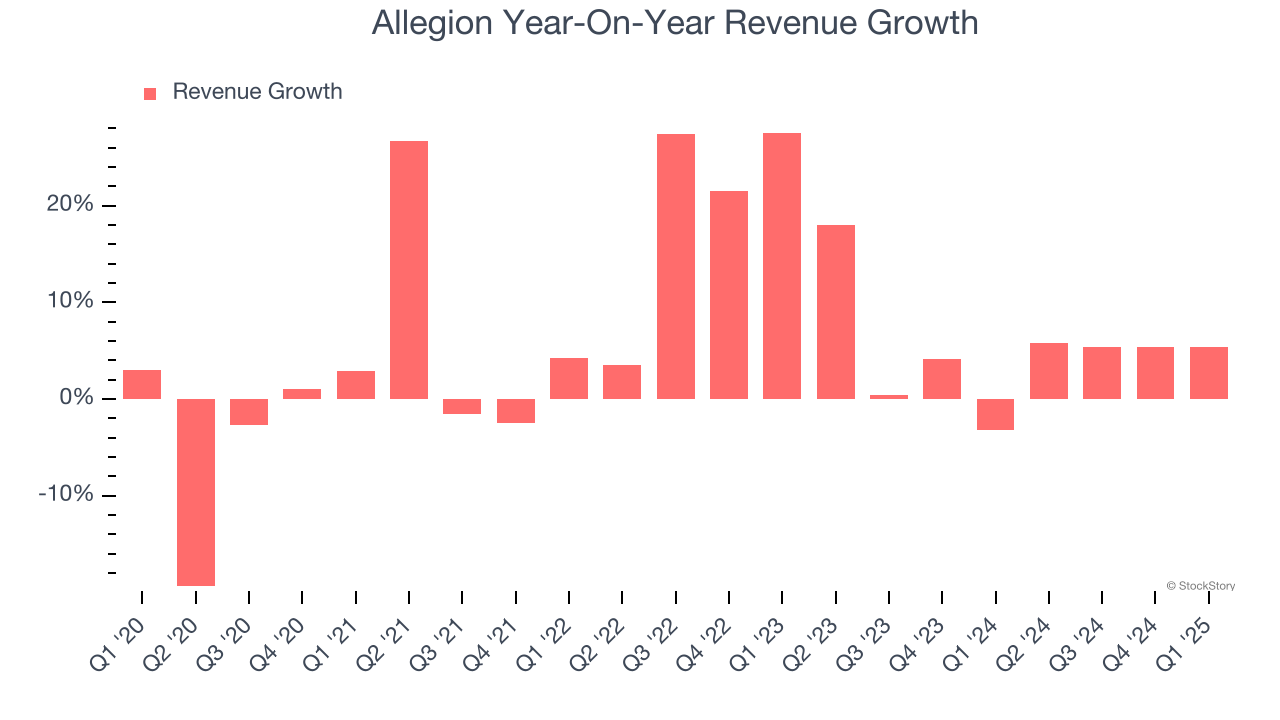

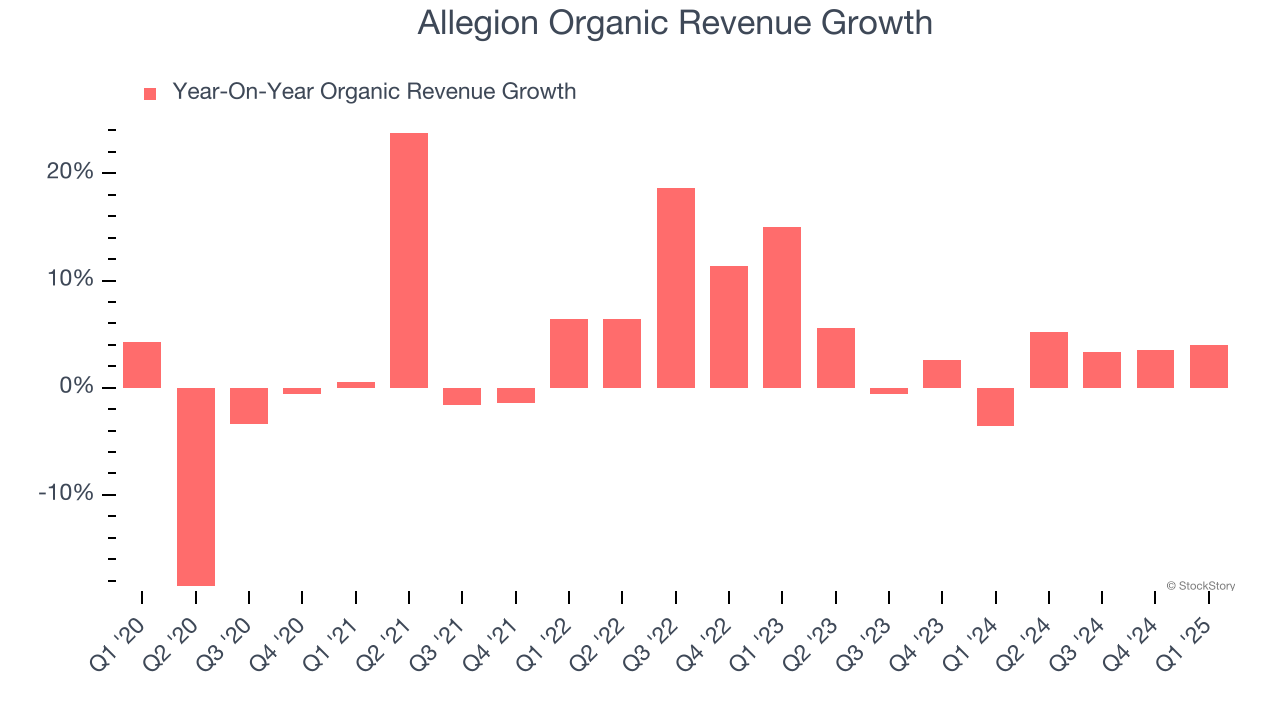

- Organic Revenue rose 4% year on year (-3.6% in the same quarter last year)

- Market Capitalization: $10.91 billion

Company Overview

Allegion plc (NYSE:ALLE) is a provider of security products and solutions that keep people and assets safe and secure in various environments.

Electrical Systems

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Allegion’s 5.9% annualized revenue growth over the last five years was tepid. This fell short of our benchmark for the industrials sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Allegion’s annualized revenue growth of 4.9% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

Allegion also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Allegion’s organic revenue averaged 2.5% year-on-year growth. Because this number is lower than its normal revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, Allegion reported year-on-year revenue growth of 5.4%, and its $941.9 million of revenue exceeded Wall Street’s estimates by 2%.

Looking ahead, sell-side analysts expect revenue to grow 2.1% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Allegion has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 19.2%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Allegion’s operating margin rose by 2.6 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, Allegion generated an operating profit margin of 20.9%, up 1.6 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

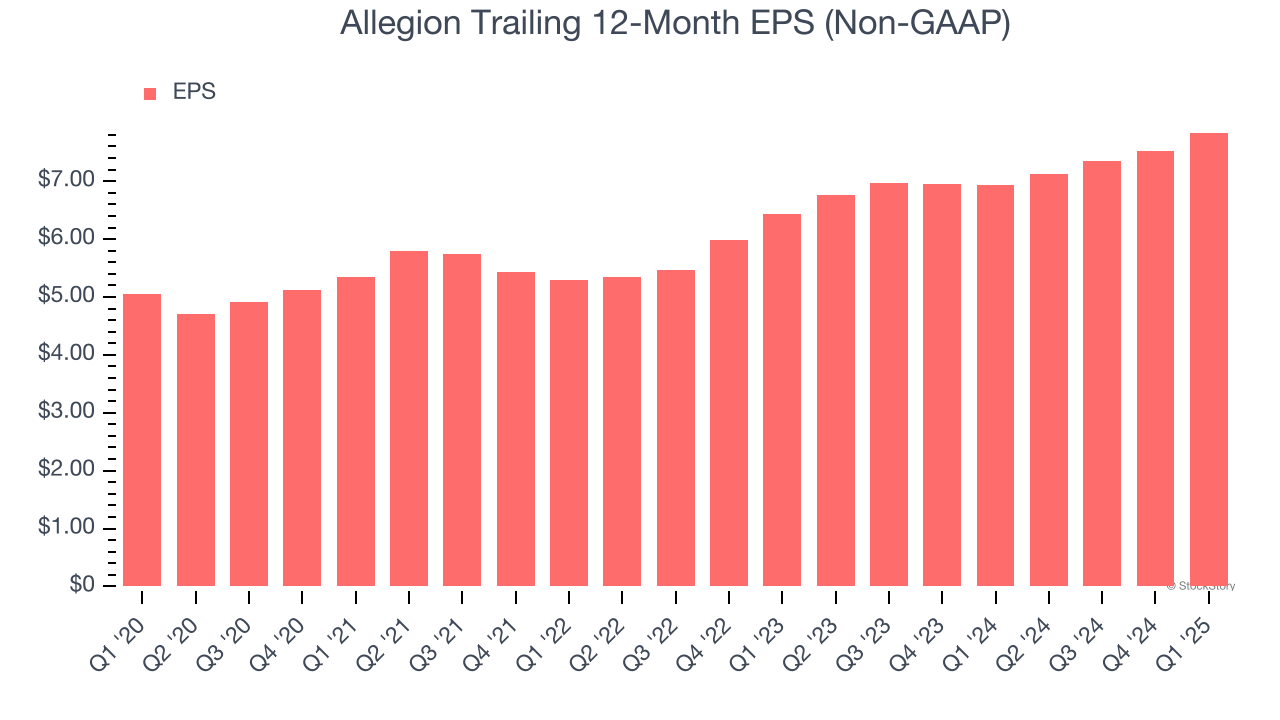

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Allegion’s EPS grew at a decent 9.2% compounded annual growth rate over the last five years, higher than its 5.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

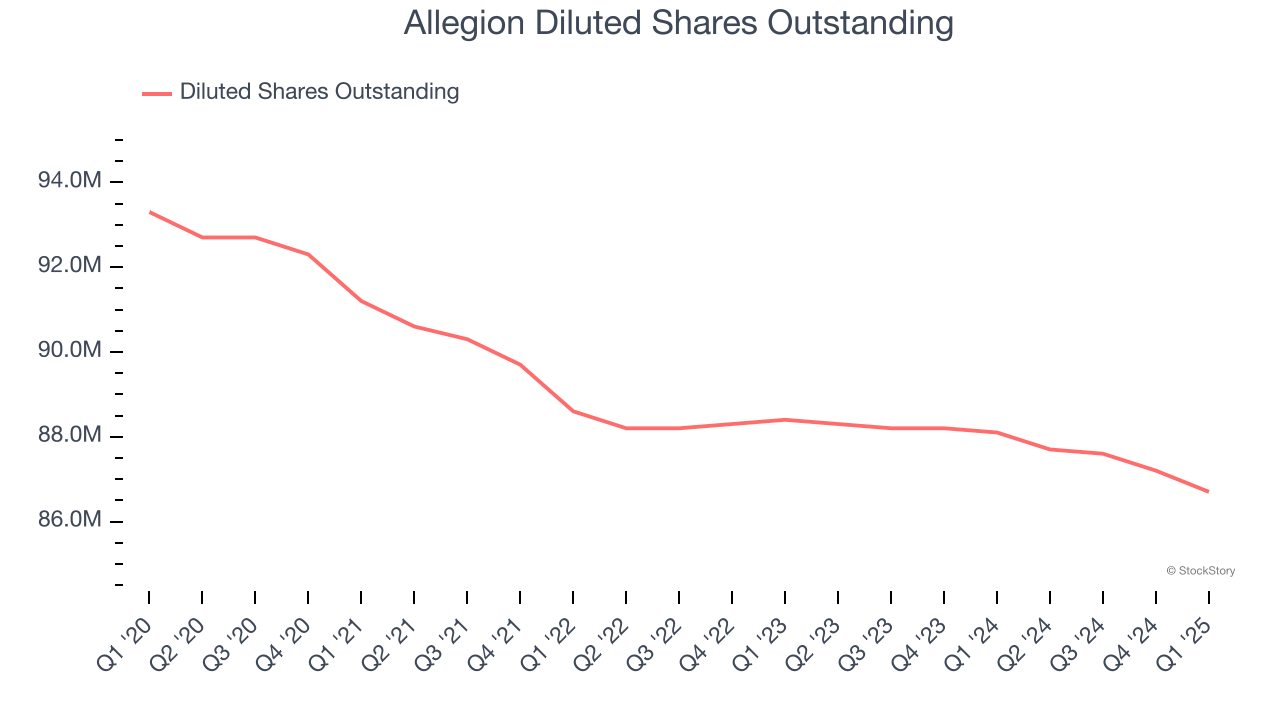

We can take a deeper look into Allegion’s earnings to better understand the drivers of its performance. As we mentioned earlier, Allegion’s operating margin expanded by 2.6 percentage points over the last five years. On top of that, its share count shrank by 7.1%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Allegion, its two-year annual EPS growth of 10.4% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q1, Allegion reported EPS at $1.86, up from $1.55 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Allegion’s full-year EPS of $7.84 to stay about the same.

Key Takeaways from Allegion’s Q1 Results

We enjoyed seeing Allegion beat analysts’ revenue and EPS expectations this quarter. Looking ahead, full-year EPS guidance was maintained. This can sometimes cause some pessimism, as the market wonders why the 'beat' wasn't flowed through to guidance Said differently, a comfortable EPS beat in the quarter should mean raising full-year guidance because lack of a raise implies a lowering of the rest of the year's outlook. The stock traded down 2% to $124 immediately after reporting.

So do we think Allegion is an attractive buy at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.