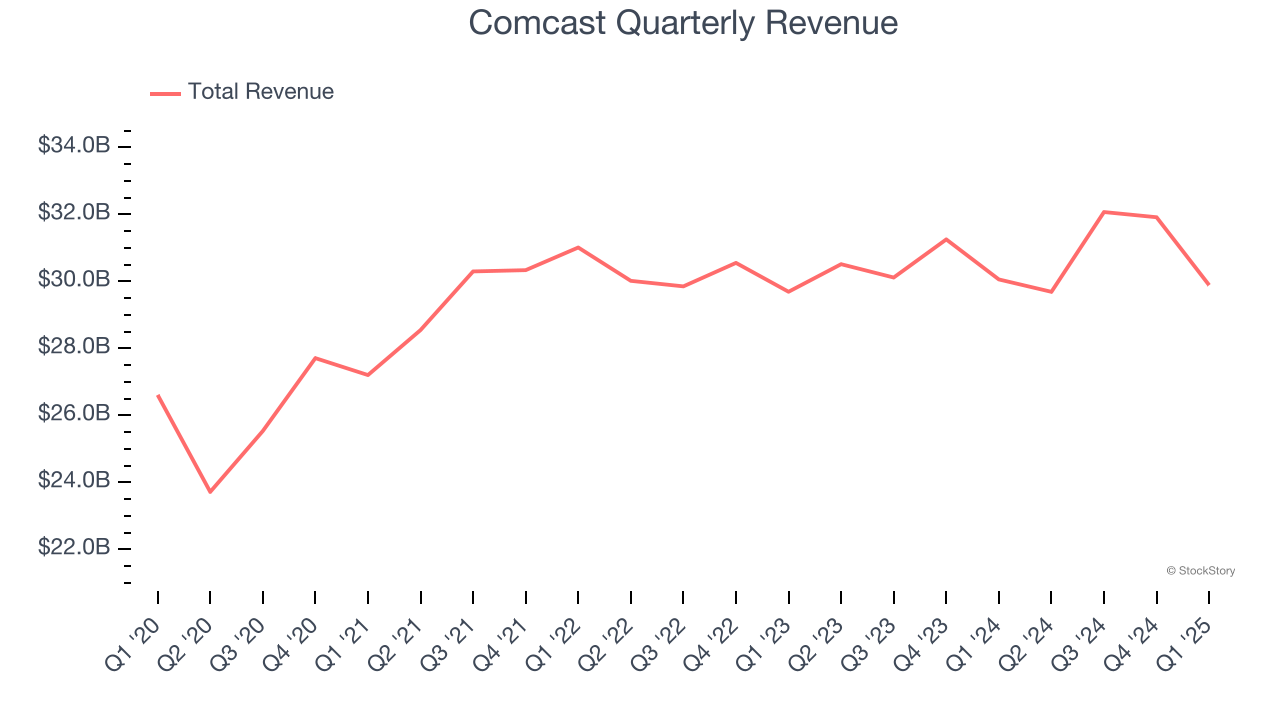

Telecommunications and media company Comcast (NASDAQ:CMCSA) met Wall Street’s revenue expectations in Q1 CY2025, but sales were flat year on year at $29.89 billion. Its non-GAAP profit of $1.09 per share was 9.9% above analysts’ consensus estimates.

Is now the time to buy Comcast? Find out by accessing our full research report, it’s free.

Comcast (CMCSA) Q1 CY2025 Highlights:

- Revenue: $29.89 billion vs analyst estimates of $29.8 billion (flat year on year, in line)

- Adjusted EPS: $1.09 vs analyst estimates of $0.99 (9.9% beat)

- Adjusted EBITDA: $9.53 billion vs analyst estimates of $9.13 billion (31.9% margin, 4.4% beat)

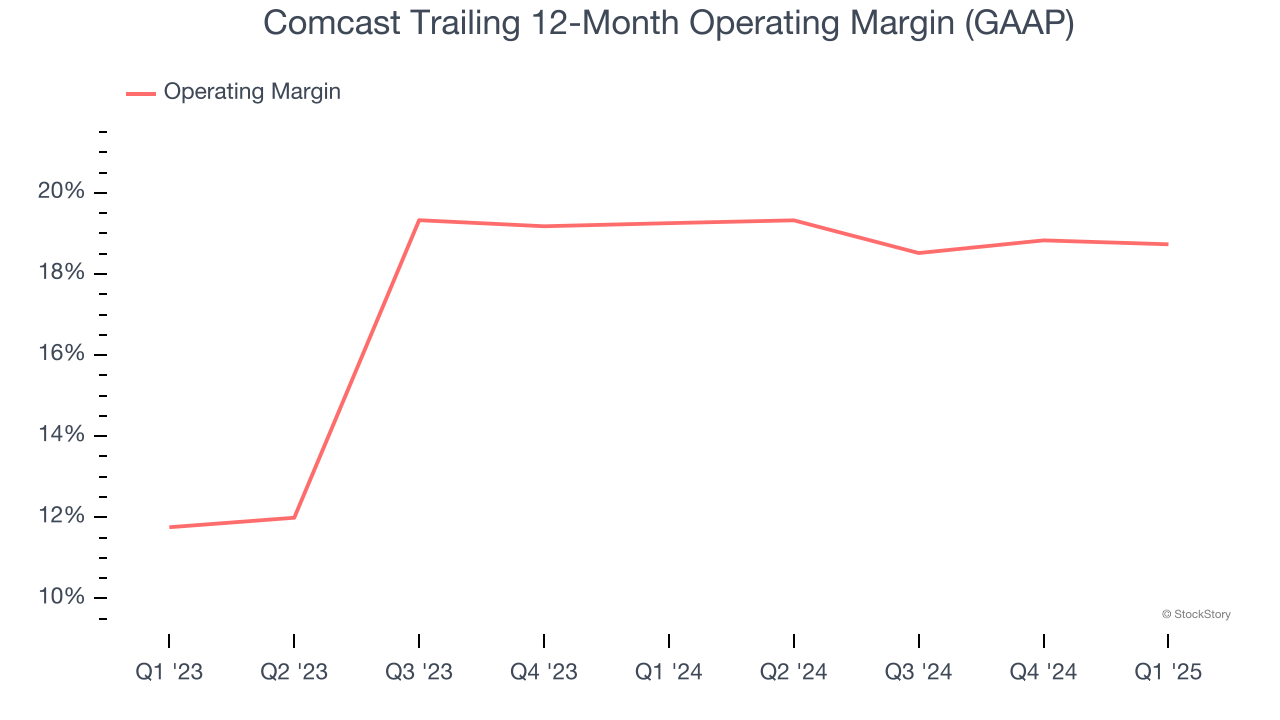

- Operating Margin: 18.9%, in line with the same quarter last year

- Free Cash Flow Margin: 18.1%, up from 15.1% in the same quarter last year

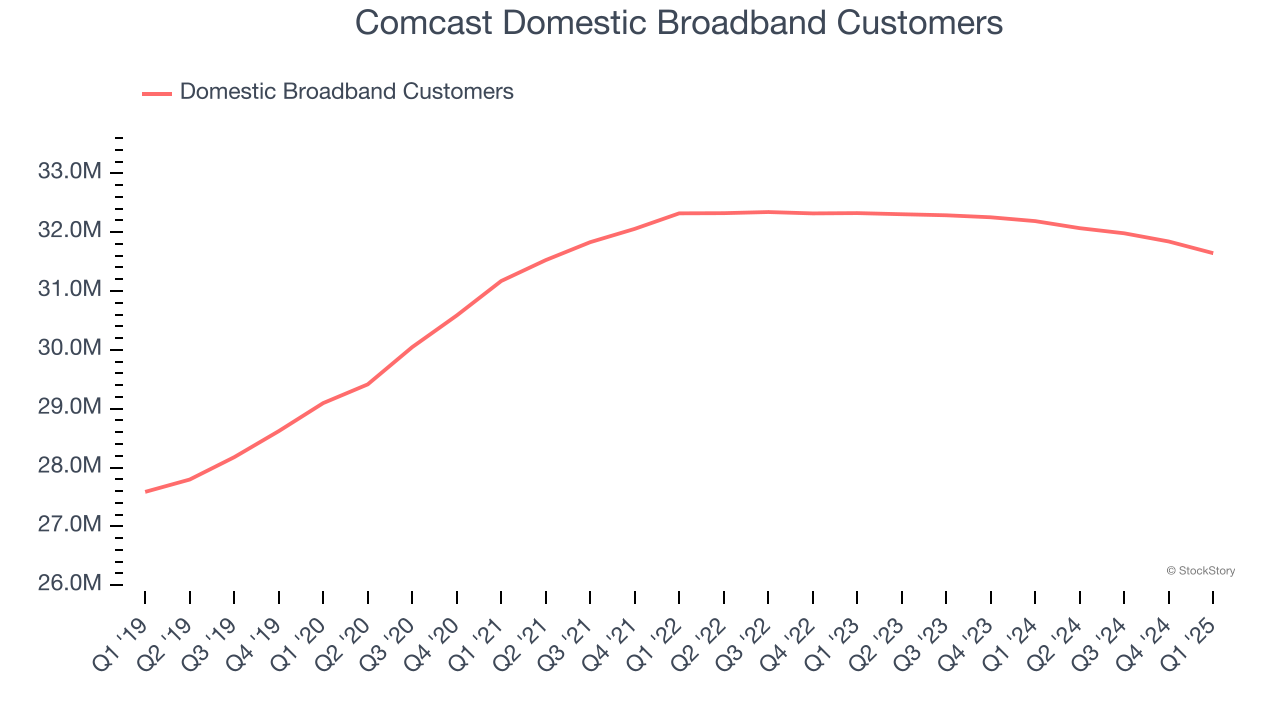

- Domestic Broadband Customers: 31.64 million, down 545,000 year on year

- Market Capitalization: $130.3 billion

“We had strong financial results in the first quarter, growing Adjusted EPS mid-single digits and generating $5.4 billion of free cash flow while investing in our six growth businesses and returning $3.2 billion to shareholders," said Brian L. Roberts, Chairman and Chief Executive Officer of Comcast Corporation.

Company Overview

Formerly known as American Cable Systems, Comcast (NASDAQ:CMCSA) is a multinational telecommunications company offering a wide range of services.

Wireless, Cable and Satellite

The massive physical footprints of cell phone towers, fiber in the ground, or satellites in space make it challenging for companies in this industry to adjust to shifting consumer habits. Over the last decade-plus, consumers have ‘cut the cord’ to their landlines and traditional cable subscriptions in favor of wireless communications and streaming video. These trends do mean that more households need cell phone plans and high-speed internet. Companies that successfully serve customers can enjoy high retention rates and pricing power since the options for mobile and internet connectivity in any geography are usually limited.

Sales Growth

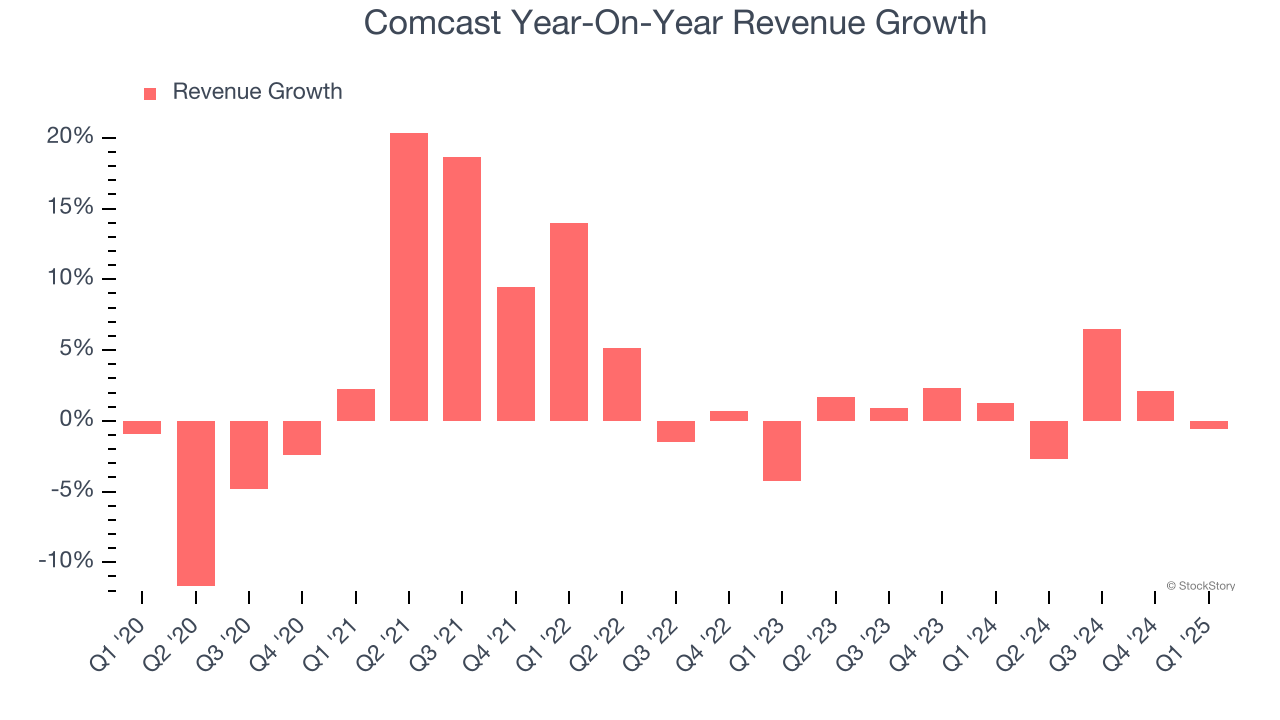

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Comcast’s sales grew at a weak 2.6% compounded annual growth rate over the last five years. This fell short of our benchmarks and is a tough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Comcast’s recent performance shows its demand has slowed as its annualized revenue growth of 1.4% over the last two years was below its five-year trend.

Comcast also discloses its number of domestic broadband customers and domestic video customers, which clocked in at 31.64 million and 12.1 million in the latest quarter. Over the last two years, Comcast’s domestic broadband customers were flat while its domestic video customers averaged 12% year-on-year declines.

This quarter, Comcast’s $29.89 billion of revenue was flat year on year and in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection doesn't excite us and implies its newer products and services will not accelerate its top-line performance yet.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Comcast’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 19% over the last two years. This profitability was top-notch for a consumer discretionary business, showing it’s an well-run company with an efficient cost structure.

In Q1, Comcast generated an operating profit margin of 18.9%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

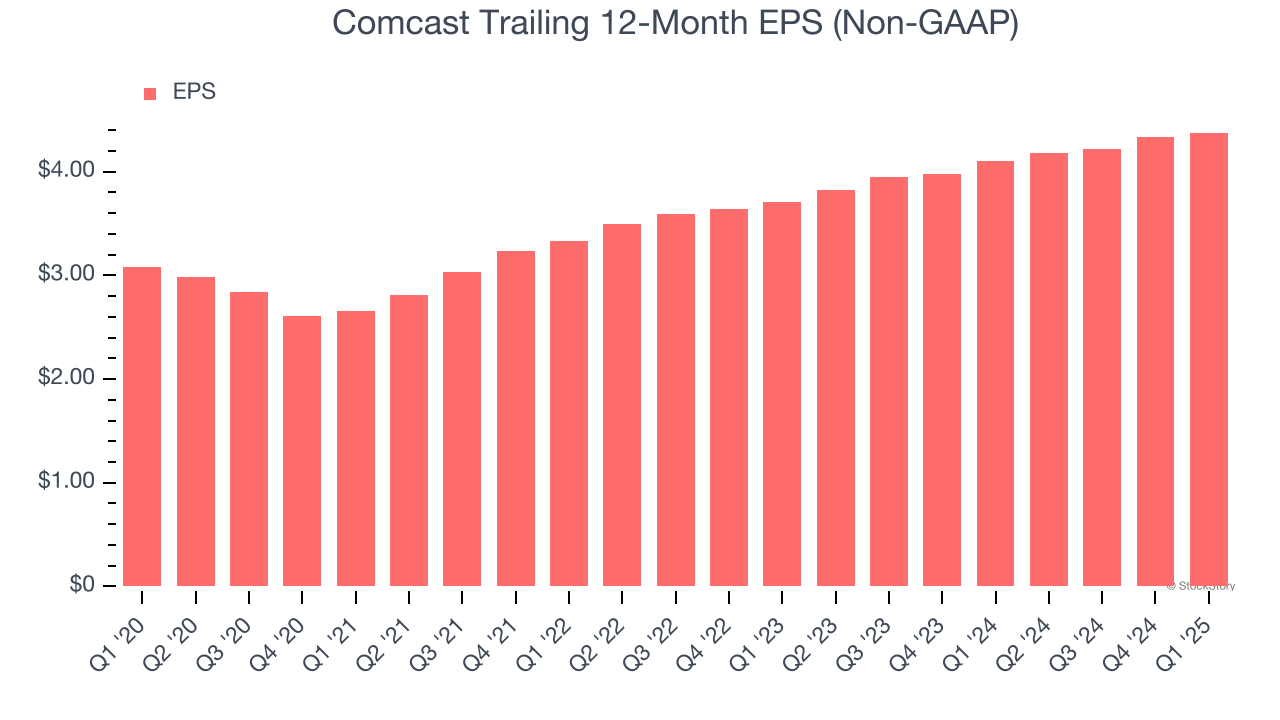

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Comcast’s EPS grew at an unimpressive 7.3% compounded annual growth rate over the last five years. This performance was better than its flat revenue but doesn’t tell us much about its business quality because its operating margin didn’t expand.

In Q1, Comcast reported EPS at $1.09, up from $1.04 in the same quarter last year. This print beat analysts’ estimates by 9.9%. Over the next 12 months, Wall Street expects Comcast’s full-year EPS of $4.38 to stay about the same.

Key Takeaways from Comcast’s Q1 Results

It was encouraging to see Comcast beat analysts’ EPS expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Overall, this quarter had some key positives, but shares traded down 3.4% to $33.24 immediately after reporting.

Big picture, is Comcast a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.